Manage Commercial Real Estate Risk with CoStar Risk Analytics

Connect to the Most Comprehensive,

Mature CRE Risk Analytics Platform in the Industry

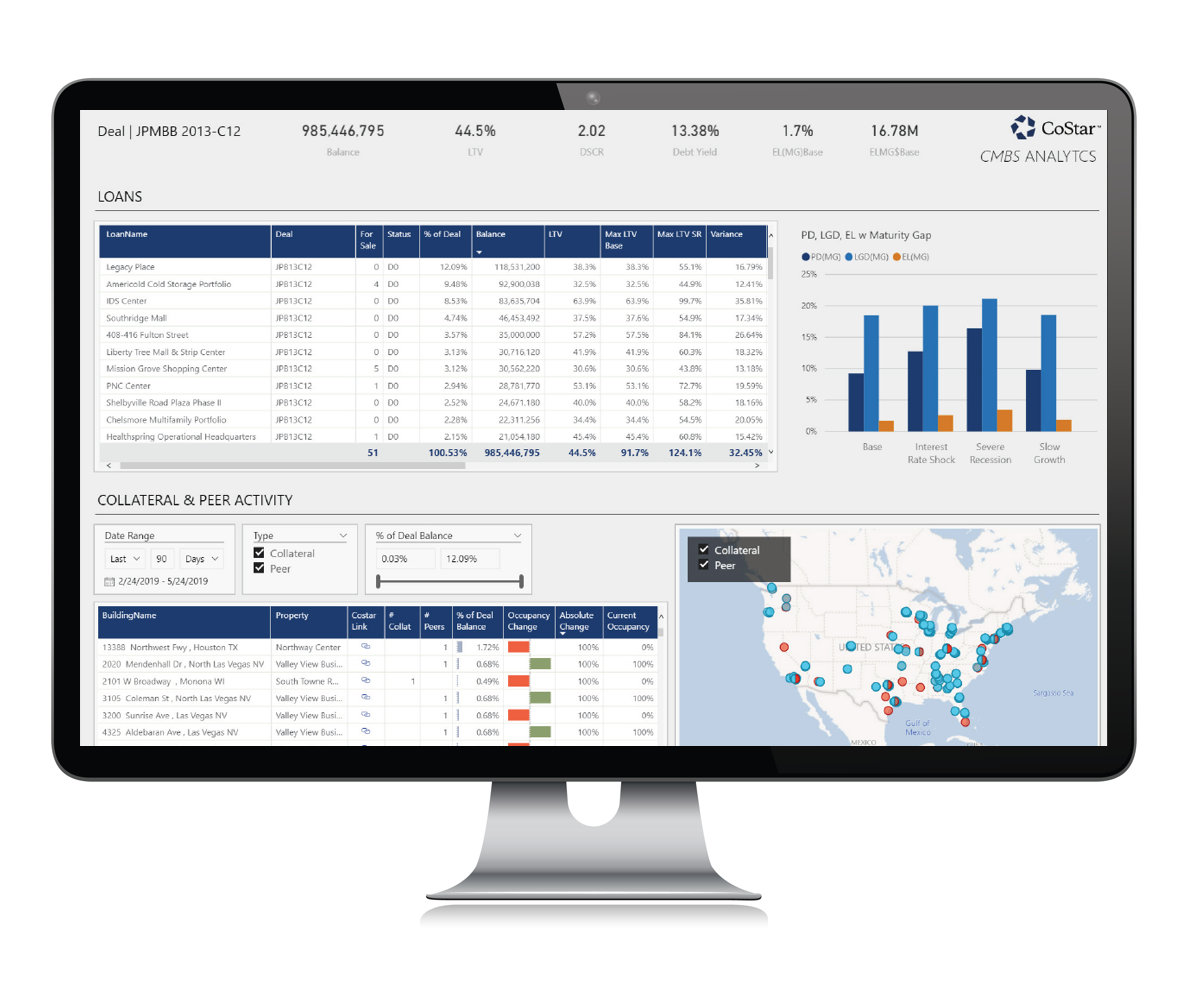

CMBS AdvantageTM Dashboard

Looking for a Regulatory and Risk Management Solution?

The CoStar Compass credit default model is the most mature in the industry. Clients have relied on it for over 15 years to determine probability of default, loss given default and expected loss throughout loan terms and at maturity.

Looking for a Better Way to Monitor Your Portfolio?

We deliver a powerful CRE (commercial real estate) Risk Management Business Intelligence via a single platform, which includes research and market analytics, our Compass mature credit default model and over 400 fields, all mapped seamlessly to each property within your portfolio.

Want an Advantage in the CMBS Market?

CoStar integrates its own best-in-class CRE data, research and market analytics with INTEX's CMBS data, the Compass mature credit default model, and over 500 fields. All mapped directly to each CMBS deal, loan, and collateral property to create a powerful CMBS Investor Product.